So there is a trope that I have seen around on the internet that points to 1971 as a major tipping point in the US economy. There is even a website about this point, filled with lots of graphs that I can't confirm the accuracy of: https://wtfhappenedin1971.com/

Basically, starting around the 1970s, it seems like there was a sharp divergence in economic growth and wage growth, increased inflation, and an increase in income inequality. It seems like this narrative is commonly used to argue that divorcing the dollar from the gold standard is the cause of these changes. I know the gold standard is not generally regarded as a good thing among mainstream economists, although it has plenty of rabid fans of course.

So my questions are: is it accurate that there was some major shift in the US economy in the 1970s, which caused wage growth to stagnate relative to GDP? Can this be attributed to any specific cause or causes? If so, what?

Edited to add: Since obviously a lot of things happened in 1971, I would say I am maybe most interested in why it seems like wage growth suddenly started to not keep up with overall economic growth starting around then.

Really interesting question, but I wonder ultimately whether it’s better asked of another subreddit. For example, I see at least one graph attributed to Emmanuel Saez, an economist, and I’m familiar with it (and the general tenor of this page) from his and Piketty’s work on wealth inequality, also grounded in economics. While I’m not familiar with their rules I wonder whether r/AskEconomics would be a better fit?

However, I can speak to one graph — the growth in incarceration that appears to start in the early 1970s. That trend is very real, and reflects what sociologists & criminologists refer to as “mass incarceration,” the sharp increase in American prison populations and imprisonment rates (people in prison per 100,000 people) over the preceding half-century. To answer why this happened, I would very strongly recommend the National Resource Council’s Growth of Incarceration in the United States. Note that while the book itself is $75(!) the eBook is free.

Travis and Western (who chaired the group that edited the book) argue for a number of causes, including policy shifts toward uniformity and certainty in sentencing, which led to mandatory terms of incarceration (“mandatory minimums”) and the end of early release policies like parole (through “truth in sentencing”). A prime example is the Rockefeller Drug Laws, 1973, which imposed sharp prison terms for drug offenses. These policies were perceived as key responses to crime, which had risen sharply during the 1960s. The national murder rate reached 10 per 100,000 in 1974; by comparison it was roughly half of that in 2014. (Note that while there is a large literature on the relationship between crime and imprisonment in the United States, it is beyond the scope of this sub.)

Those trends are historical fact, but underlying them are many, many other factors. I would call upon a postwar America historian to flesh those out, as that takes me beyond my expertise as a student of history. It’s worth noting that Travis and Western point to shifting political attitudes — consider the “war on drugs” (“declared” in 1971) — and broad economic trends, like deindustrialization in urban centers, which dried up sources of stability and opportunity for predominantly young men. Notably, those underlying causes have their roots well before 1971.

I hope some of this is helpful!

There are some theories which don't exactly synchronize across the entire span of time (say, competition from China, which didn't really kick in until the 1990s). This doesn't mean alternate factors aren't relevant -- something can keep decreasing but not keep to the same dominant force the entire time -- but still the current best thinking is that employers formed a monopsony.

For those who haven't heard of it, let's start with a more familiar word: monopoly. That's when, through whatever forces of coincidence and/or greed, companies merge together enough that consumers get no choices, causing the price of goods to go up, since where else are they going to buy them?

Monopoly can be thought of as "multiple buyers, single seller". Monopsony is then: "single buyer, multiple sellers".

Why is this bad? Because: when there is only one buyer, they get to set the price. Where else are the companies going to sell their product? This is essentially the situation with employers and wages.

Imagine employers are buyers, trying to purchase time from workers. Now imagine there is only one viable employer in a particular area. Now, they have no need to raise wages, because there are no other choices of employers.

This is arguably what has been happening in the US since the late 70s, just with many more industries and with ramifications tossed out over much a longer span of time.

(If you're wondering, knives sharpened, if this is a leftist or a rightist argument, well, kind of neither; I've heard it mentioned by people on both ends of the spectrum, and doesn't fit nicely into a political box. It suggests unions ought to be stronger -- we'll get to that -- but it also suggests Competition is Good. It also suggests income inequality is bad and harmful for the economy overall. Getting into the weeds here would be for the wrong sub, but I'm trying to pre-empt at least a few questions.)

Now, back to 1971. Unfortunately, that (and the years immediately after) are probably not the best to consider the absolute start of a trend, just because of the utter chaos wrought by the gold standard being given the final boot, as alluded to, but the energy crisis in general. As I wrote about in regards to an episode of The Simpsons:

...in the 1972-1974 period in the United States both food and energy prices rose (there was a Saudi Arabian-led oil embargo on countries thought to support Israel in the Yom Kippur War) and a second food price hike kicked off more inflation from the 1978-1980 range ... The end result was an average inflation of 6.85% over the decade, eye-popping compared to the prior two decades (2.38 and 2.56 percent respectively) and at some points the inflation reached double digits.

If you'd like the raw economist-plays-with-data attack this paper picks up starting in 1978. For some more concrete historical ideas:

Union numbers, already starting to tilt, began their serious dive in the 70s; their peak was really in the 1930s and their doom was potentially marked by the Taft-Hartley Act of 1947, which opened the possibility for right-to-work states (there are now 28 of them; this means employees can get a job without joining the respective union). In the 70s they were seriously affected by the same food/energy crisis as everyone else, and unions tend to be good at pointing out monopsony. Reagan in 1981 put a further nail in the coffin by firing the striking air traffic control works (while technically an illegal strike from government workers, this still gave the green light for anti-union forces, which I've written about in detail here).

a 1976 paper (“Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure") argued against the current public firm structure, that shareholders were not being considered by managers who only looked after themselves; this and related forces led to stock-based compensation, but data suggests this didn't improve conditions and simply led to a focus on short term growth (hitting quarterly earnings) as opposed to long term growth. While there was also the rise of the workers owning stock, they did not have the ability to steer companies.

Corporate raiders of the 1980s and beyond started doing hostile takeovers and essentially squeezing out assets for profit, mangling companies in the process. (Most infamously is Carl Icahn, who took the airline TWA in 1985, sold off its good parts, and essentially burned it to the ground.)

To condense things: dissolution of companies started with the energy crisis of the 70s, continued with high interest rates causing trouble through the Carter administration and into the 80s, while simultaneously a switch to stock-based compensation (intended to make managers more accountable to the needs of the company) made them more short-term focused and hurt company health in the longer term, while simultaneously through the 80s there were on the scale of thousands of leveraged buyouts, some of the investors being bad caretakers of the company indeed.

With two factories for a worker to choose from, they can easily quit and move to the other one if they offer better wages, hence an upward trend of wages. When enough companies go under that there's only one factory to work at, the trend stops.

And this doesn't even touch upon the more recent trends of increasing government-hands-off approach monopoly simultaneously causing monopsony issues, the foreign manufacturing that I mentioned at the top, and what I might argue is the worst trend for monopsony, non-compete clauses. They quite directly discourage job-hopping with a whopping 18% of current workers in US under such a clause.

I just wanted to speak a bit towards that website. I think that specifically what it is trying to argue (with extremely varying degrees of good arguments) is that all these social and economic changes can be traced back to the United States ending gold convertibility in 1971. I say the arguments are of extremely varying degrees because as has been pointed out here, some things like crime are trends that stretched back into the 1960s, some things like deregulation more properly start around the 1980s, and even something like inflation is complicated by the fact that it was already rising in the 1960s, and was drastically impacted by things like the 1973 and 1979 Oil Shocks.

The decision on August 15, 1971 is often referred to in this context as removing the US dollar from the gold standard, and that's true to a certain extent, but a very specific one. It was the end of the Bretton Woods system, which had been established in 1944, with 44 countries among the Allied powers being the original participants. This system essentially created a network of fixed exchange rates between currencies, with member currencies pegged to the dollar and allowed a 1% variation from those pegs. The US dollar in turn was pegged to $35 per gold ounce. At the time the US owned something like 80% of the world's gold reserves (today it's a little over 25%).

The mechanics of this system meant that other countries essentially were tying their monetary policies to US monetary policy (as well as exchange rate policy obviously, which often meant that US exports were privileged over other countries'). The very long and short is that domestic US government spending plus the high costs of the Vietnam War meant that the US massively increased the supply of dollars in this fixed system, which meant that for other countries, the US dollar was overvalued compared to its fixed price in gold. Since US dollars were convertible to gold, these other countries decided to cash out, meaning that the US gold reserves decreased basically by half in the decade leading up to 1971. This just wasn't sustainable - there were runs on the dollar as foreign exchange markets expected that eventually it would have to be devalued against gold.

This all meant that after two days of meeting with Treasury Secretary John Connally and Budget Director George Schultz (but noticeably not Secretary of State William Rogers nor Presidential Advisor Henry Kissinger), President Richard Nixon ordered a sweeping "New Economic Policy" on August 15, 1971, stating:

"“We must create more and better jobs; we must stop the rise in the cost of living [note: the domestic annual inflation rate had already risen from under 2% in the early 1960s to almost 6% in the late 1960s]; we must protect the dollar from the attacks of international money speculators.”"

To this effect, Nixon requested tax cuts, ordered a 90-day price and wage freeze, a 10% tariff on imports (which was to encourage US trading partners to revalue their own currencies to the favor of US exports), and a suspension on the convertibility of US dollars to gold. The impact was an international shock, but a group of G-10 countries agreed to new fixed exchange rates against a devalued dollar ($38 to the gold ounce) in the December 1971 Smithsonian Agreement. Speculators in forex markets however kept trying to push foreign currencies up to their upper limits against the dollar, and the US unilaterally devalued the dollar in February 1973 to $42 to the gold ounce. By later in the year, the major world currencies had moved to floating exchange rates, ie rates set by forex markets and not by pegs, and in October the (unrelated, but massively important) oil shock hit.

So what 1971 meant: it was the end of US dollar convertability to gold, ie the US "temporarily" suspended payments of gold to other countries that wanted to exchange their dollars for it. What it didn't mean: it wasn't the end of the gold standard for private US citizens, which had effectively ended in 1933 (and for good measure, the exchange of silver for US silver certificates had ended in the 1960s). It also wasn't really the end of the pegged rates of the Bretton Woods system, which hobbled on for almost two more years. It also wasn't the cause of inflation, which had been rising in the 1960s, and would be massively influenced by the 1970s energy crisis, which sadly needs less explaining in 2022 than it would have just a few years ago.

It also really doesn't have much to do with social factors like rising crime rates, or female participation in the workforce. And it deceptively doesn't really have anything to do with trends like the US trade deficit or increases in income disparity, where the changes more obviously happen around 1980.

Also, just to draw out the 1973 Oil Shock a little more - a lot of the trends around economic stagnation, price inflation, and falls in productivity really are from this, not the 1971-1973 forex devaluations, although as mentioned the strain and collapse of Bretton Woods meant that US exports were less competitive than they had been previously. But the post 1945 world economy had been predicated on being fueled by cheap oil, and this pretty much ended overnight in October 1973: even when adjusted for inflation, the price essentially immediately tripled that month, and then doubled again in 1979. The fact that the economies of the postwar industrial world had been built around this cheap oil essentially meant that without major changes, industrial economies were vastly more expensive in their output (ie, productivity massively suffered), and many of the changes to make industries competitive meant long term moves towards things like automation or relocating to countries with cheaper input costs, which hurt industrial areas in North America and Western Europe (the Eastern Bloc, with its fossil fuel subsidies to its heavy industries, avoided this until the 1990s, when it hit even faster and harder).

" I know the gold standard is not generally regarded as a good thing among mainstream economists,"

I just want to be clear here that no serious economist considers a gold standard a good thing. This is one of the few areas where there is near universal agreement among economists. The opinion of economists on the gold standard is effectively the equivalent of biologists' opinions on intelligent design.

So, most political economists will tell you it's the shift off of the Gold Standard but will warn you off of phrases like "good" or "bad" because those are normative descriptions. Yes, the US was on the Gold Standard prior to 1971 but, perhaps more critically, the move off of the Gold Standard precipitates (a few years later) the end of the post-war Bretton Woods system in which many of the world's currencies were pegged to the US Dollar.

As an aside, Bretton Woods is why the plot of the James Bond movie/novel Goldfinger doesn't make any sense today. The idea that Goldfinger could make money by buying gold in one country, transporting it to another, and then selling it seems crazy today because gold is a global commodity.

For example from 1949 to 1967 the Pound was worth exactly $2.80. In 1964 (when Goldfinger came out) an ounce of gold was $35.35 in the US or ₤12.57 in the UK. You'll note, however, that ₤12.57 (price of gold in UK) x 2.8 (pounds to dollars exchange rate) doesn't land you at $35.35 but at $35.196. That's an arbitrage opportunity, which is what Goldfinger was doing and why gold export/ownership was so tightly controlled. (The UK/US arbitrage is one of the smaller ones but it's also the easiest to find data on).

Anyway, when the US went off the Gold Standard and the Bretton Woods system ended, not only did the price of gold float against the US dollar - the price of most/every other currency in the world did too. Now, there were a lot of reasons behind this but the one that's relevant to our discussion here is the way those artificial currency exchange rates effected the cost of imported and exported goods. If the Deutschmark was artificially weak against the Dollar, for example, that made US goods like Orange Juice and Fords artificially expensive in Germany while making German goods like Volkswagens and Beer inexpensive in the United States.

That's great for Americans buying Volkswagens (and part of the reason why the VW Bug became the success it was) but it's not such a great deal for Americans making Fords or growing oranges... they can't sell their goods to overseas markets. That was by design - like much of the post-war economic order, Bretton Woods was intended to help get Europe back on its feet following the devastation of WWII, but by the 1970s much of that work had been done. A floating currency system seemed like it would balance out in the long run -- Americans would have a harder time buying imported products but American workers would benefit from fair trade with overseas markets in the form of higher wages.

That didn't work out as intended for a couple of reasons. First, the economic shocks of this shift -- often called the "Nixon Shocks" -- created a lot of short to medium term instability in the US economy. The 1970s were characterized by stagflation and energy crises which were, in part, fueled by the reverberations of the end Bretton Woods. Second, the end of the gold standard and Bretton Woods turned finance into a global game which was significantly more complex than it had been prior. With currencies, bonds, interest rates, and commodities prices all moving relative to each other an already asymmetric information economy became even more asymmetric. For a pop-take on what Wall Street looked like during the inflection point of the 1980s, check out Liars Poker by Michael Lewis. Critically, during this time, we saw Wall Street Trader go from a low-status job with almost no meaningful job requirements to one of the most elite, well compensated, and bombastic careers in the United States. That reflected a massive movement of capitol from the generally risk-averse middle class of the post-war years into the pockets of an increasingly rarefied 1% and 0.1%.

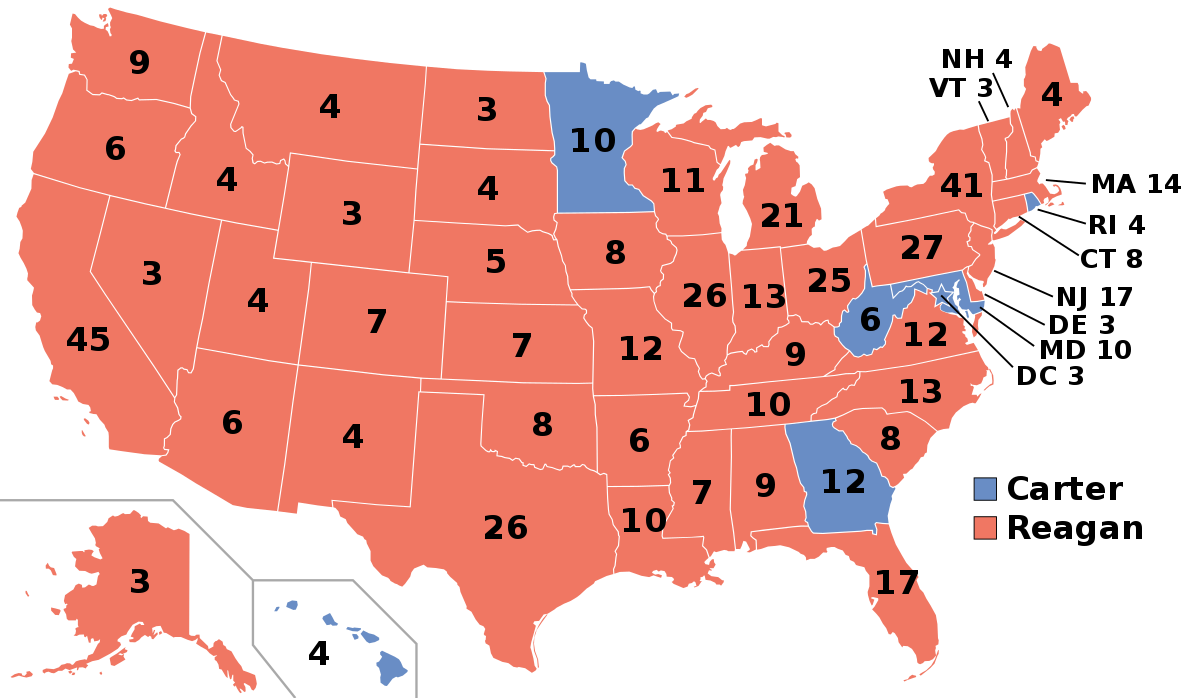

This instability was politically devastating to the party in power at the time which happened to be the Democrats. Carter's election in 1976 came just in time for the chickens of 1971 to come home to roost. That's not to say that none of the Carter era economic problems were Carter's fault, but many were not. This brought Reagan into the White House in 1981 with a HUGE electoral mandate (seriously, look at this map; it's a bloodbath) based on a platform of "Trickle Down Economics." Reagan's success quickly transformed this into the dogma of the Republican Party. George HW Bush, who characterized the policy as "voodoo economics" when he was running against Reagan for the nomination in 1980 had fully embraced it by the time of his own nomination in 1988 when he famously promised "read my lips: no new taxes."

So, by the end of the 1980s you have a United States which has shrugged off its post-war consumer advantages and in which a major party now embraces an economic policy which prioritizes economic stratification. Meanwhile US foreign policy, especially after the end of the Cold War, increasingly prioritizes the lowering of trade barriers under the assumption that economic interdependence and democratic peace theory will make "the world safe for democracy." In so doing, however, the United States creates conditions in which it is both profitable and easy to move much of the manufacturing sector which supported the rise of the 20th century middle class overseas to places with dramatically lower costs of living.

As industry leaves for cheap labor in South East Asia, Americans find themselves holding the short end of the Bretton Woods stick. The benefits to American manufacturing don't matter when America no longer manufactures. Farming, the other major American export industry and which in 1950 employed about 20% of American workers, employed just 2% of Americans by the 1990s.

That takes us pretty much to the present day. Since then, if anything, we've seen the continued growth of the Finance sector in the US economy which contributes significantly to the concentration of capitol.

Globalization.

Leaving the Breton Woods agreement and the international gold standard was only one part of a larger string of events.

Keep in mind, the US enjoyed unprecedented prosperity in the 1950s and 1960s due to successful wartime and post-war policies like the New Deal and GI Bill, along with the destruction of the productive capacity and massacre of the prime-age male workforce of competing nations. So comparing the ‘50s and ‘60s to any period is fraught. Trends were favorable for (white male) Americans, unsustainably so. (Note: I’m not comparing absolute levels here I’m comparing growth rates like wage growth, home ownership growth, etc.)

The 1970s were a major tipping point for globalization. This included removing gold standard, which probably made lots of foreign economies which were being held back by fixed exchange rates more competitive.

When there is more foreign competition, domestic conditions change.

Wages are competed downwards while capital returns are not affected as much because capital can be invested across borders. Things related to wages - like ability to live independently and incarceration rates - also move. Keep in mind though, the life during the ‘50s and ‘60s should not probably be taken as the norm… but moves up or down are always relative to some other time period.

Keep in mind that globalization meant huge improvements in quality of life for people in less developed areas (including massive numbers of people in Asia). So things may have looked slightly less rosy for certain parts of the US population but average global income and living standards improved massively in the decades that followed.

Other somewhat “odd” charts are interesting in this context. For example growth of chicken vs beef makes sense as chicken is far more efficient in terms of space and food fed to the livestock vs calories and nutrients produced. Red meat is very inefficient. In a world of global growth and competition, move towards efficiency makes sense.

Many charts, like inequality and productivity-wage decoupling go back to ideas I mentioned before: it’s better to be a capital owner than an owner of labor (I.e. a worker) in a globalized and competitive world.

Also, we can’t take the events of the early 1970s in a vacuum. Nixon and Ford were followed by Carter, who was ineffectual, and then Reagan. Reagan destroyed unions through judicial appointments which led to court cases that de-fanged organized labor, severely limiting its ability to counterbalance the power of business. The US also shifted to a services economy (again related to globalization but also a separate phenomenon), while the education system failed to adapt, leaving those without means to pay a lot for education behind. I’m abstracting away from a lot but education, lack of organized labor, and returns to capital vs labor in globalized world are some of the major reasons for inequality rising. Though there are many and it hasn’t been fully solved.

The 1970s were certainly a tipping point. Partially they look like more of a tipping point because many characteristics of the US economy of the ‘60s were probably unsustainable. But there certainly was a long term, secular shift underway to a more globalized world with that year looking in particular like an inflection point and with many many implications.

{kind=link}

{kind=link}